Funding and Debt Management

The NTMA is responsible for borrowing on behalf of the Government and managing the National Debt in order to ensure liquidity for the Exchequer and to minimise the interest burden over the medium term.

Issuing Longer-Dated Debt

Debt Service Costs Lower

€6.1bn |

Interest on the National Debt fell to €6.1bn in 2017, a decline of almost 10% compared to 2016 and close to 20% below the 2014 peak. |

|

|---|---|---|

12% |

Interest costs accounted for 12% of Exchequer tax revenue in 2017, compared with 14% in 2016. |

Gross National Debt at End-2017

Figures may not total due to rounding.

MARKET REVIEW

The further strength and recovery of the Irish economy continues to be viewed favourably by investors in Irish Government bonds. This progress, along with credit rating upgrades and the ongoing ECB quantitative easing measures, were positive influences on the Irish bond market throughout 2017.

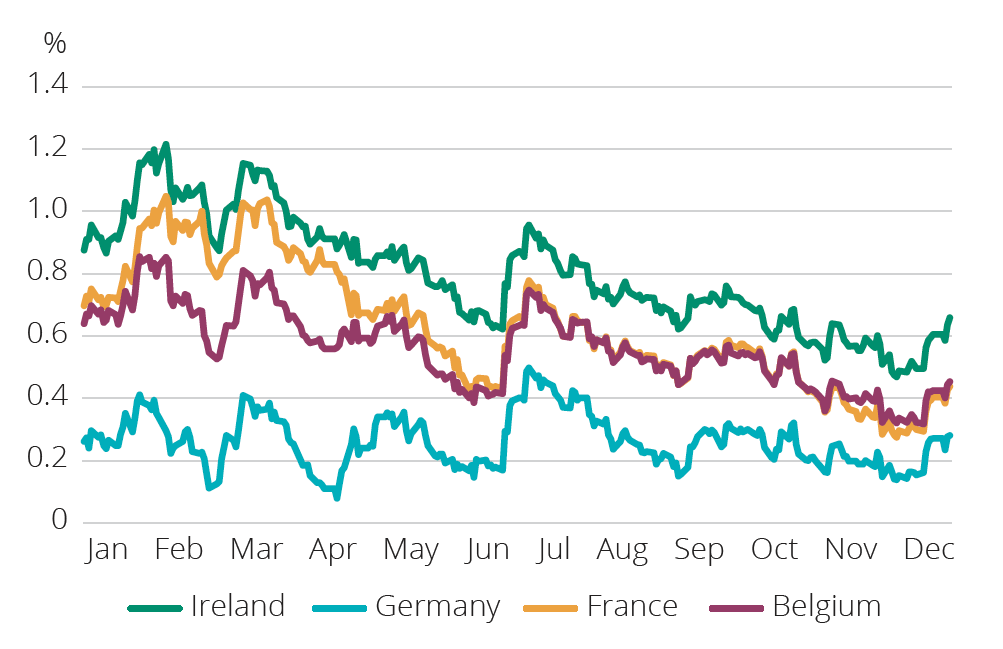

The yield on Ireland’s 2026 bond started the year at close to 0.90% and rose to a peak of 1.22% in February. The early months of the year saw increased volatility and higher yields, before a reduction in perceived risk from the French presidential election led yields lower. The summer months were influenced by uncertainty over Brexit negotiations, leading to an uptick in yields. However, yields resumed their downward trend in the second half of the year, influenced by the announced ECB extension of the quantitative easing programme, albeit at a reduced pace. This saw Ireland’s 2026 bond closing the year at 0.66%.

In 2017, Ireland’s 2026 bond yield tightened from a high of over 90 basis points above the German equivalent, to almost 40 basis points by year-end. It was trading 20 basis points higher than France and Belgium at year-end. Irish Government bond yields are now viewed as closely correlated with these countries.

2026 Government Bond Yields

Source: Bloomberg

ECB Quantitative Easing

The ECB introduced quantitative easing measures in March 2015. The programme, whereby national central banks purchase government bonds in the secondary market, is officially known as the Public Sector Purchase Programme (PSPP). Between March 2015 and December 2017, the ECB purchased €1.9 trillion in eurozone public sector bonds. Irish Government bonds accounted for just over €25bn of this. The PSPP has been extended until at least September 2018, although at a reduced level. Monthly purchases under ECB programmes, reduced from a peak of €80bn to €60bn from April 2017, and were further reduced to €30bn per month from January 2018.

FUNDING ACTIVITY

Long-Term Funding

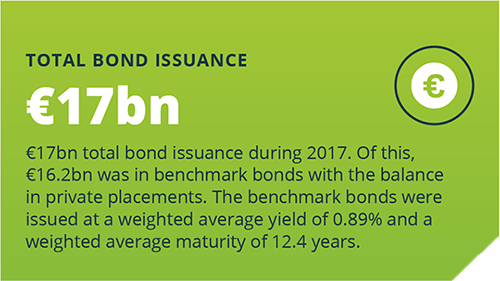

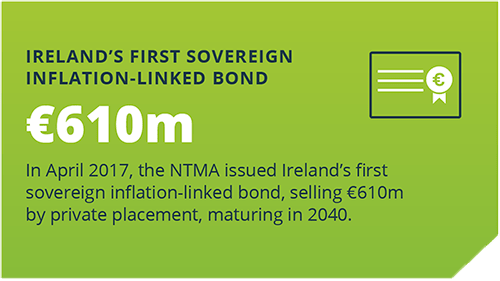

The NTMA completed a total of €17bn of long-term issuance during 2017. Of this, €16.2bn was in benchmark bonds. These had a weighted average yield of 0.89% and a weighted average maturity of 12.4 years. In addition, Ireland’s first inflation-linked bond was issued by private placement in April 2017, raising €610m. Two further private placements of long-dated bonds of €100m each were also completed during the year.

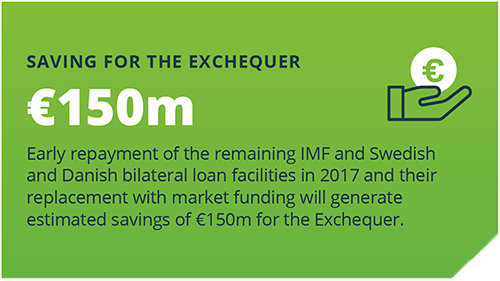

The NTMA’s original stated funding range for the year was €9bn to €13bn. However, additional issuance was undertaken to fund the early repayment of loans from the IMF, Sweden and Denmark totalling €5.5bn. This will reduce the Exchequer debt service bill by an estimated €150m over the otherwise remaining term of the loans.

This issuance contributed further to the NTMA’s strategy of locking in low interest rates and longer maturities. Over the 2015-2017 period, the NTMA issued almost €40bn in new benchmark bond funding at a weighted average yield of just over 1% and a weighted average maturity of almost 14 years.

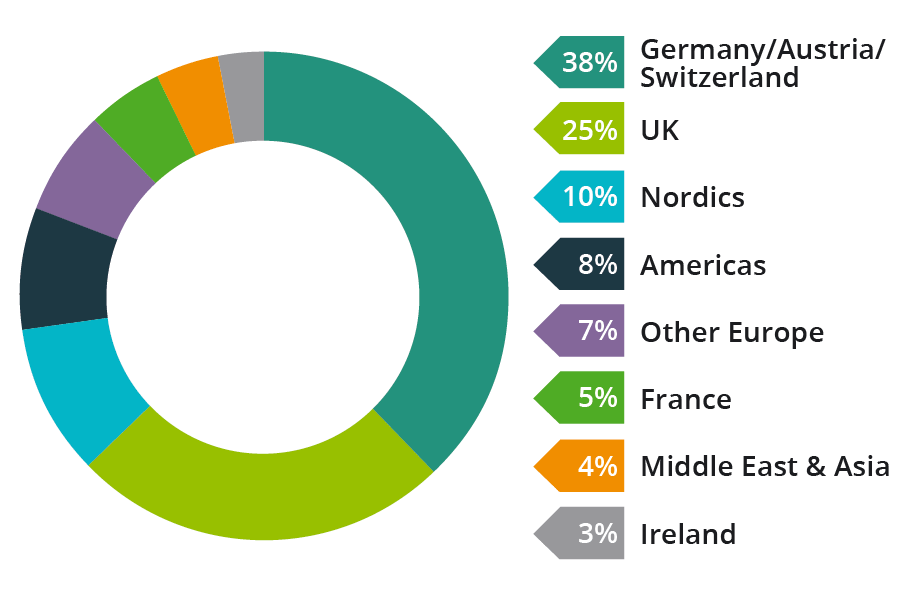

The NTMA undertook two bond syndications in 2017. The first was a new 20-year bond issued in January, with €4bn being sold at a yield of 1.73%. There was strong interest, with overseas investors taking 97% of the amount issued. Purchases were spread across a range of investor types including fund managers, banks, pension and insurance funds and central banks.

20-Year Bond Syndication by Geographic Area

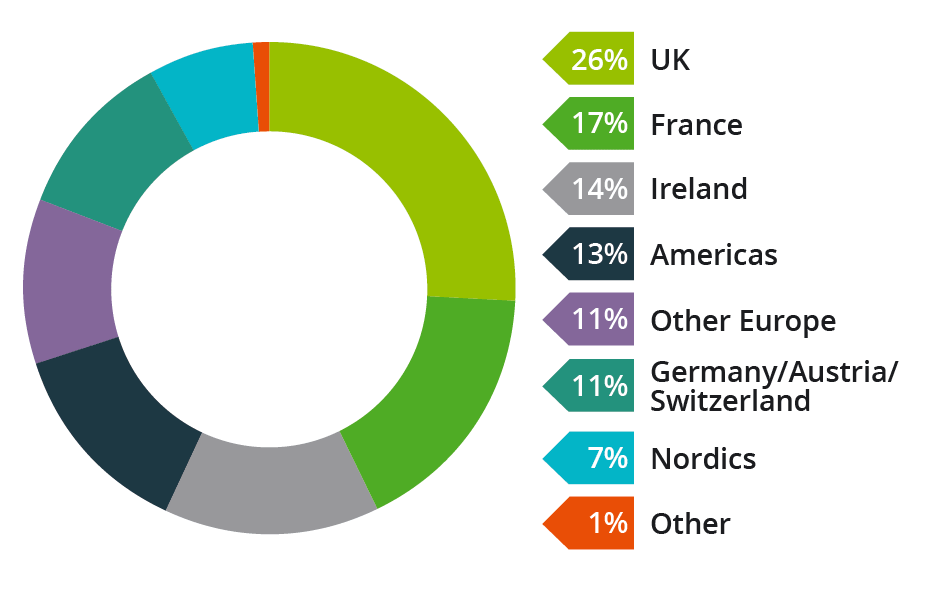

The second syndication of the year took place in October. This was a new 5-year bond issued to fund the early repayment of loans from the IMF, Sweden and Denmark, with €4bn being sold at a negative yield of -0.01%. Again, there was strong interest from a broad range of investors with overseas investors taking over 85% of the issue.

5-Year Bond Syndication by Geographic Area

The NTMA also held seven bond auctions during the year, raising almost €8.2bn. These were all dual bond auctions, with a choice of two bonds on offer in each auction.

NTMA Bond Auctions 2017

| Bond Name |

Auction Size €m* |

Yield % |

Bid- Cover Ratio |

|---|---|---|---|

| 9 February | |||

| 0.8% Treasury Bond 2022 | 600 | 0.09 | 2.0 |

| 1% Treasury Bond 2026 | 650 | 1.03 | 2.0 |

| 9 March | |||

| 1% Treasury Bond 2026 | 850 | 1.05 | 1.7 |

| 2% Treasury Bond 2045 | 400 | 2.19 | 2.0 |

| 12 April | |||

| 3.9% Treasury Bond 2023 | 633 | 0.20 | 1.8 |

| 1% Treasury Bond 2026 | 805 | 0.94 | 1.6 |

| 8 June | |||

| 1% Treasury Bond 2026 | 805 | 0.72 | 2.3 |

| 2% Treasury Bond 2045 | 345 | 1.92 | 1.8 |

| 13 July | |||

| 0.8% Treasury Bond 2022 | 500 | -0.01 | 2.3 |

| 2% Treasury Bond 2045 | 250 | 1.95 | 2.1 |

| 14 September | |||

| 1% Treasury Bond 2026 | 554 | 0.69 | 2.6 |

| 1.7% Treasury Bond 2037 | 518 | 1.65 | 1.7 |

| 9 November | |||

| 1% Treasury Bond 2026 | 800 | 0.54 | 2.0 |

| 2% Treasury Bond 2045 | 450 | 1.70 | 1.5 |

| * includes proceeds of non-competitive auctions. | |||

Ireland’s first inflation-linked bond was issued in April 2017, raising €610m.

The bond was issued as a private placement. It will mature in April 2040 and has an annual coupon of 0.25%. The interest payments and principal repayment are linked to the Eurostat Harmonised Index of Consumer Prices (HICP) for Ireland, excluding tobacco.

The demand for this bond came from investors who have Irish inflation-linked liabilities. In the past, they may have used inflation-linked bonds issued by other eurozone members as a substitute.

The decision to issue an inflation-linked bond for the first time is in line with the NTMA’s stated intention to diversify its issuance over the long term and increase the pool of investors in Irish bonds. Inflation-linked bonds attract a different source of investor demand from the fixed-rate bonds that are the mainstay of the NTMA’s issuance.

Early Repayment of IMF, Sweden and Denmark Loans

In December 2017, Ireland completed the early repayment of the full outstanding IMF loan facility and the bilateral loans from Sweden and Denmark. An amount of SDR3.8bn1 (c. €4.5bn) was repaid to the IMF, while €1bn was repaid in respect of the bilateral loans from Sweden (€0.6bn) and Denmark (€0.4bn). This early repayment reduces the Exchequer debt service bill, by an estimated €150m over the otherwise remaining term of the loans.

As part of the EU-IMF Programme of Financial Support entered into in late 2010, Ireland borrowed SDR19.5bn (c. €22.5bn) from the IMF. The NTMA repaid early SDR15.7bn (just over €18bn) over the period December 2014 to March 2015. With these further early repayments, the IMF loan facility has been fully repaid ahead of schedule.

The remaining Programme related debt is as follows:

- European Financial Stabilisation Mechanism (EFSM): €22.5bn

- European Financial Stability Facility (EFSF): €18.4bn

- UK Bilateral Loan: £3.2bn (c. €4bn)

In 2017, the NTMA bought back approximately €2bn of bonds due to mature in 2018-2020. This reduction in the volume of near-term debt maturities, replacing them with longer-dated bonds, contributes to the strategy of locking in low interest rates and lengthening the maturity of the debt.

A total of €4bn nominal of Floating Rate Bonds held by the Central Bank were also bought back during 2017. These were replaced with medium to long-term fixed rate market funding. The total outstanding balance of the Floating Rate Bonds stood at €15.5bn at end-2017, compared with €25bn originally issued in 2013.

Short-Term Funding

The NTMA broadened its short-term issuance base by both maturity and volume in 2017. There was €2bn in Treasury Bills outstanding at end-2017, an increase from €1bn at end-2016. Four auctions were held during the year, each with a 12-month maturity.

The NTMA also maintained Ireland’s Multi-Currency Euro Commercial Paper (ECP) programme in 2017. Total turnover in ECP during the year was €5.5bn and there was €0.5bn outstanding at end-2017.

As a result of the ECB’s expansionary monetary policies and the low interest rate environment, the NTMA was able to issue all Treasury Bills and ECP at negative euro-equivalent interest rates in 2017. Short-term debt was also issued in the form of Exchequer Notes and Central Treasury Notes, mainly to domestic institutional investors.

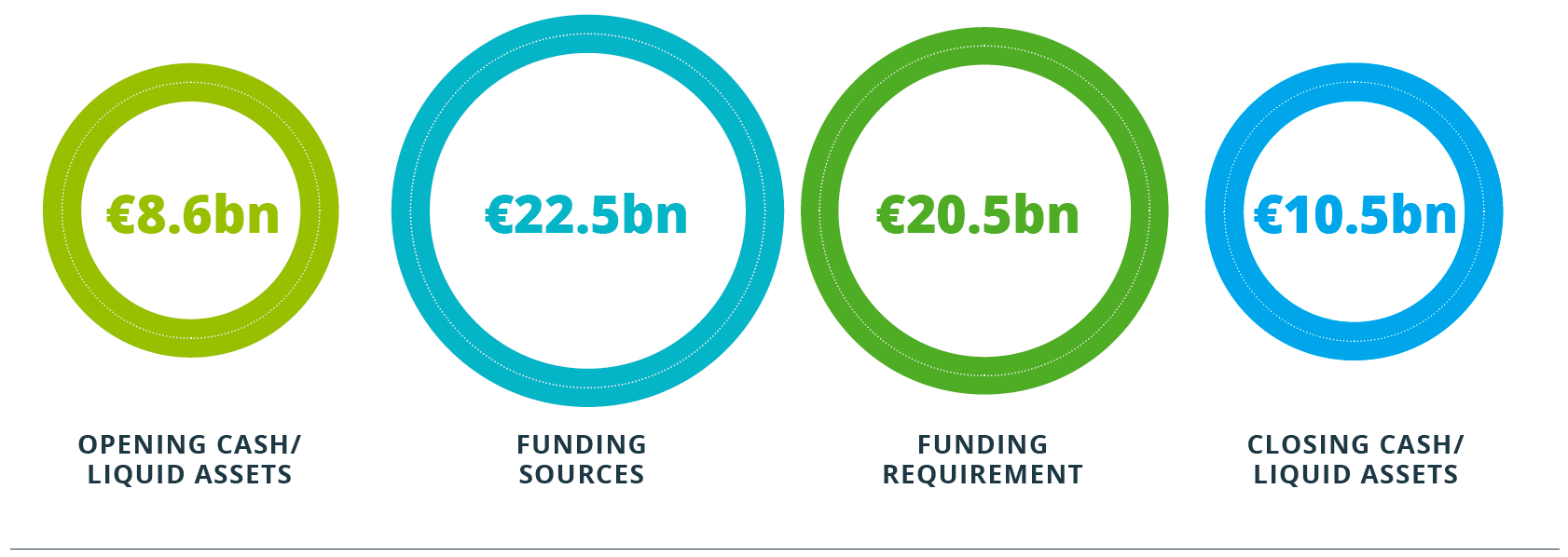

Exchequer Funding Sources and Requirements 2017

The Exchequer had cash and other short-term liquid assets of €10.5bn at end-2017 (up from €8.6bn at end-2016). 2017 bond issuance, including the inflation-linked bond, raised €17bn, while other funding sources totalled €5.5bn. This included the proceeds of the Government’s sale of part of its shareholding in AIB, short-term paper and State Savings products.

This funding was applied to fund an Exchequer Borrowing Requirement (excluding the AIB share sale proceeds) of €1.5bn, bond maturities of €6.2bn, the early repayment of EU/IMF Programme loans as well as Floating Rate Bond purchases and fixed-rate bond switches. The funding also resulted in an increase in cash balances, reflecting a continuation of the pre-funding strategy adopted by the NTMA in advance of larger redemptions over the 2018 to 2020 period.

Figures may not total due to rounding.

State Savings

State Savings is the brand name applied by the NTMA to the range of Irish Government savings products offered to personal savers. During 2017, there were net inflows of €0.3bn into the State Savings products. At end-2017, the total amount outstanding in fixed rate products and prize bonds was €17.3bn. When deposit accounts are included, this brings the year-end total to €20.4bn.

State Savings Products

| Total Outstanding at End-2017 €m |

Net Inflow/ (Outflow) in 2017 €m |

|

|---|---|---|

| Savings Bonds | 3,250 | (497) |

| National Solidarity Bonds | 4,343 | 194 |

| Savings Certificates | 6,026 | 118 |

| Instalment Savings | 503 | 5 |

| Prize Bonds | 3,170 | 278 |

| Deposit Accounts | 3,121 | 200 |

| Total | 20,413 | 298 |

| Figures may not total due to rounding. |

The current fixed interest rate offerings for the latest issues of State Savings products are detailed below.

State Savings Interest Rates

| Product | Fixed Rate Total Return % |

Annual Equivalent Rate % |

|---|---|---|

| 3-Year Savings Bond | 1.0 | 0.33 |

| 4-Year National Solidarity Bond | 2.0 | 0.50 |

| 5-Year Savings Certificate | 5.0 | 0.98 |

| 6-Year Instalment Savings | 5.5 | 0.98 |

| 10-Year National Solidarity Bond | 16.0 | 1.50 |

The variable rate on the Deposit Accounts is currently 0.15%. The variable rate of interest used to determine the value of the Prize Bonds monthly prize fund was reduced in August 2017, from 0.85% to 0.50%. The top weekly prize is €50,000, except in the last weekly draw of June and December, when the top prize is €1m.

DEBT PROFILE

General Government Debt (GGD) is a measure of the total gross consolidated debt of the State. It is the standard measure used for comparative purposes across the European Union.

National Debt is the net debt incurred by the Exchequer after taking account of cash balances and other financial assets. The primary component of General Government Debt is Gross National Debt – that is the National Debt before netting off cash and financial assets. The NTMA’s responsibilities relate to the management of the National Debt only.

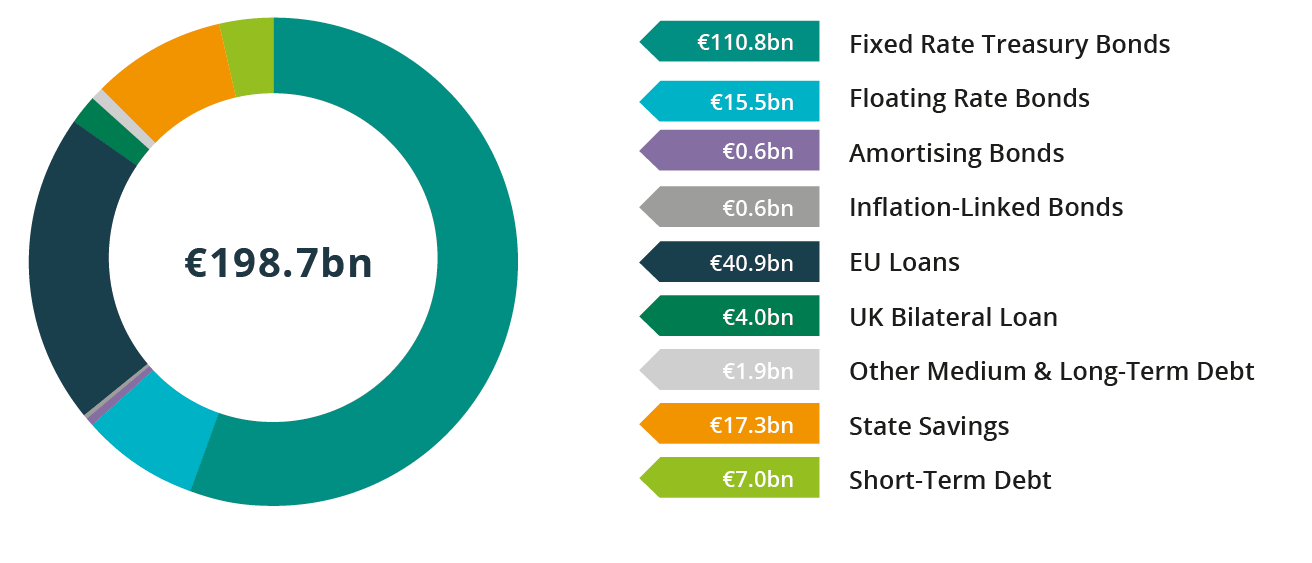

Composition of General Government Debt at End-2017

| €bn | |||

|---|---|---|---|

| Government Bonds | |||

| Fixed Rate Treasury | 110.8 | ||

| Floating Rate | 15.5 | ||

| Amortising | 0.6 | ||

| Inflation-Linked | 0.6 | ||

| Total | 127.6 | ||

| EU Loans | 40.9 | ||

| UK Bilateral Loan | 4.0 | ||

| Other Medium and Long-term Debt | 1.9 | ||

| State Savings Schemes* | 17.3 | ||

| Short-Term Debt | 7.0 | ||

| Gross National Debt | 198.7 | ||

| Less Exchequer Cash and other Financial Assets | 13.2 | ||

| National Debt | 185.5 | ||

| Gross National Debt | 198.7 | ||

| General Government Debt Adjustments | 2.6 | ||

| General Government Debt | 201.3 | ||

Figures may not total due to rounding.

*In addition to the amounts shown in the table above, State Savings Schemes also include moneys placed by depositors in the Post Office Savings Bank (POSB) which are not an explicit component of the National Debt. These funds are mainly lent to the Exchequer as short-term advances and through the purchase of Irish Government Bonds. Taking into account the POSB Deposits, total State Savings outstanding were €20.4bn at end-2017.

Source: NTMA and Central Statistics Office

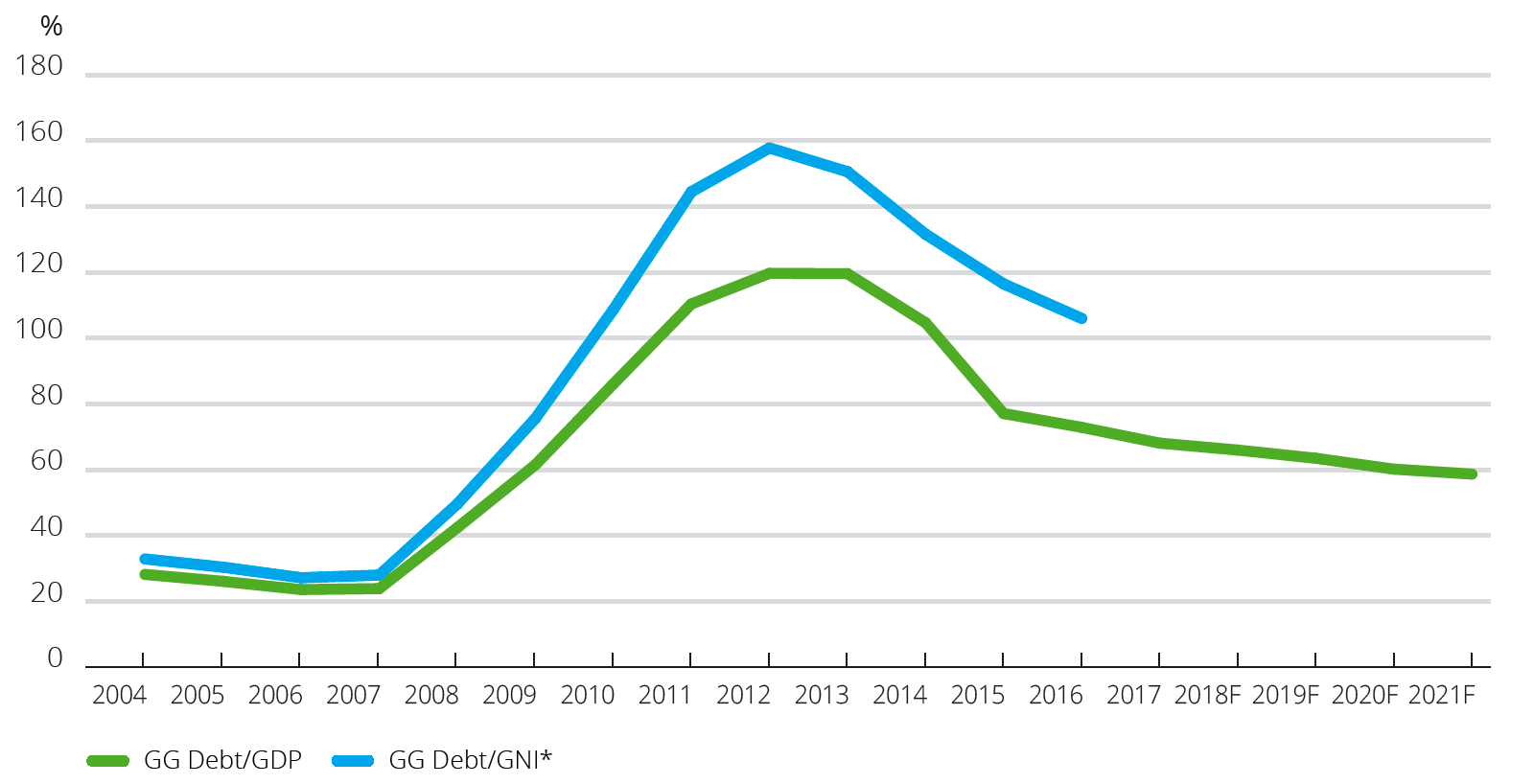

At 68%, Ireland’s ratio of GGD/GDP has fallen significantly since its peak of 120%. However, the absolute level of debt remains high. Ireland’s GGD at end-2017 was over €200bn.

The recent decline in the GGD/GDP ratio is primarily as a result of a sharp rise in GDP. In particular, Ireland’s GDP figures from 2015 onwards are highly affected by the activities of multinational companies.

Nonetheless, there is strong underlying economic activity as evidenced by employment and consumption figures. This is a positive development which improves Ireland’s debt sustainability.

GGD/GDP Ratio 2004-2021

Source: CSO and Department of Finance

The significant impact on Ireland’s GDP figures of the activities of multinational companies make the ratio of debt to GDP less reliable as an indicator of sustainability. In that context, it is worth focusing on additional metrics to obtain a clearer picture of Ireland’s debt burden.

One alternative metric is General Government Debt as a percentage of Modified Gross National Income (GNI*). GNI* is a metric created by the CSO to modify GDP for the impact of multinationals’ activities. The GGD/GNI* ratio fell from a peak of almost 158% in 2012 to 106% in 20162.

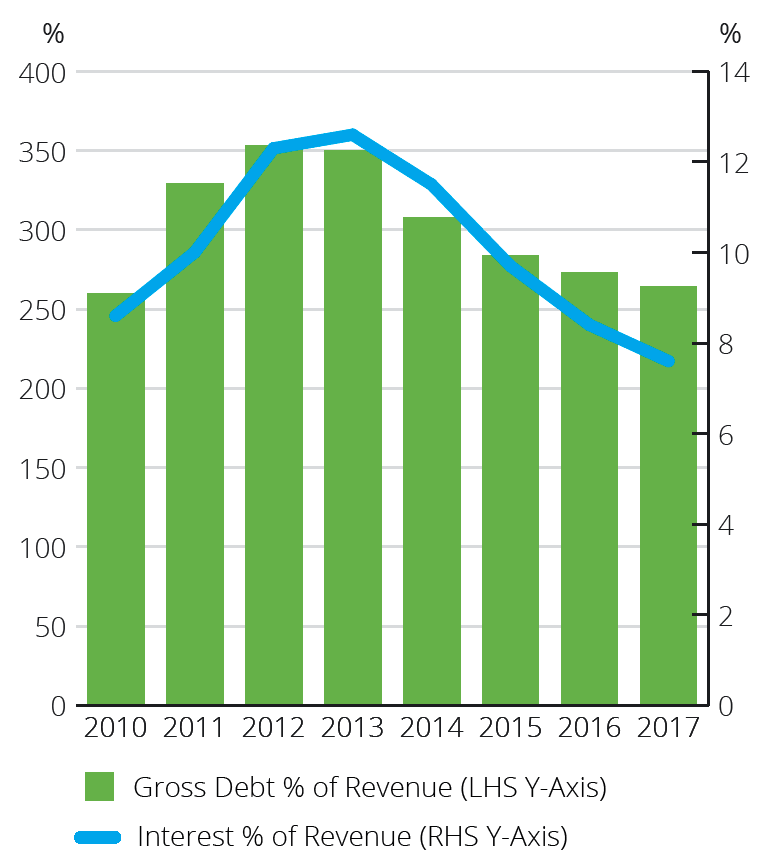

Other additional metrics measure debt and interest as a percentage of General Government Revenue. GGD as a percentage of revenue stood at 264% at end-2017, while interest as a percentage of revenue was 7.6%.

Whichever metric is used, Ireland’s debt dynamics continued to improve in 2017.

General Government Debt and Interest Metrics 2010-2017

Source: NTMA and CSO

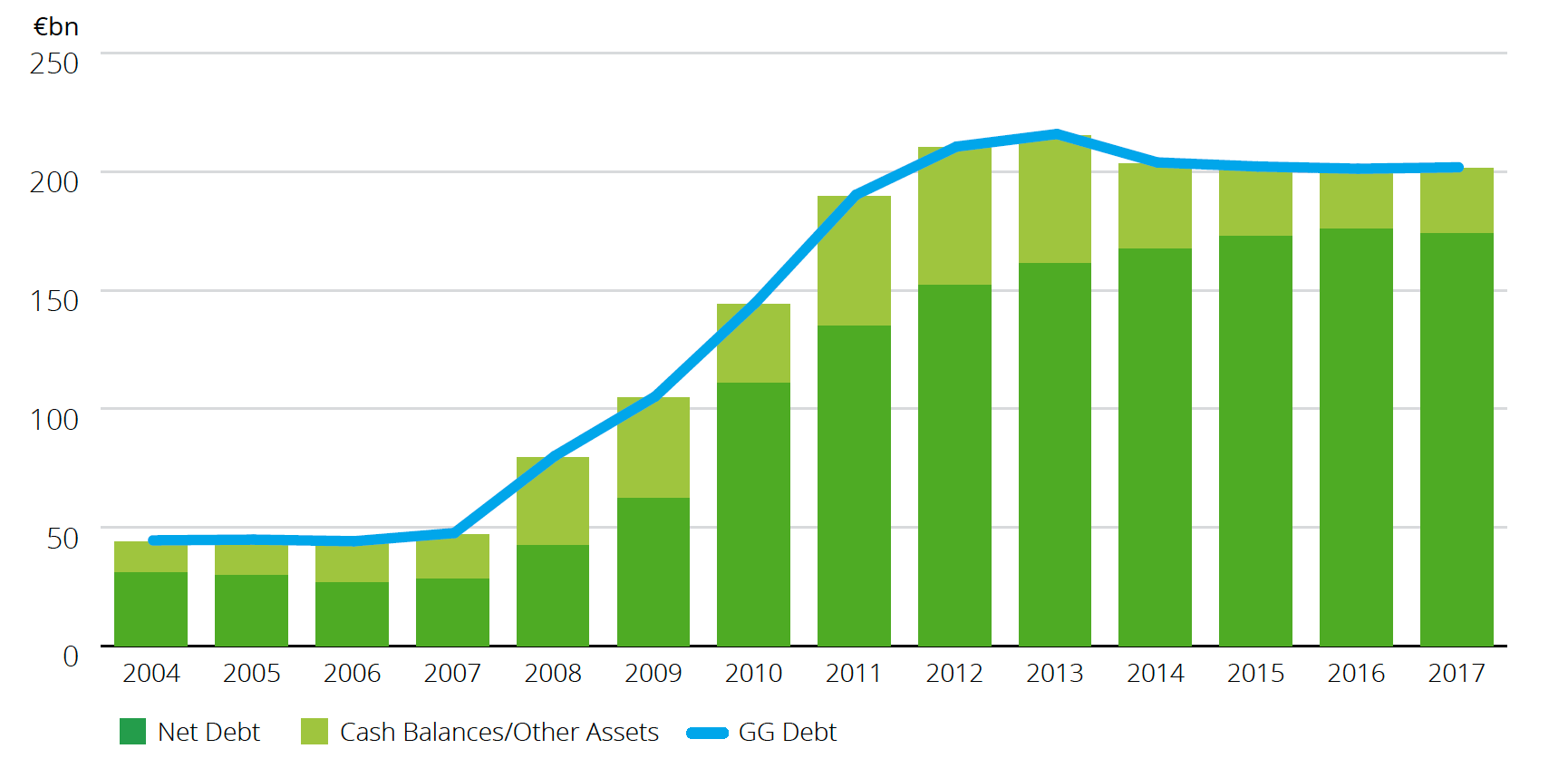

GGD is a gross measure which does not allow for the netting off of cash balances and other financial assets. However, the CSO produces an estimate of General Government Net Debt which, at end-2017, stood at €174bn or 59% of GDP. The financial assets of €27bn netted off for the purpose of calculating Net Debt include ISIF cash and non-equity investments as well as Exchequer cash and financial assets. They exclude the Government’s equity stakes in the Irish banking sector, most notably AIB.

Gross and Net General Government Debt 2004-2017

Source: CSO

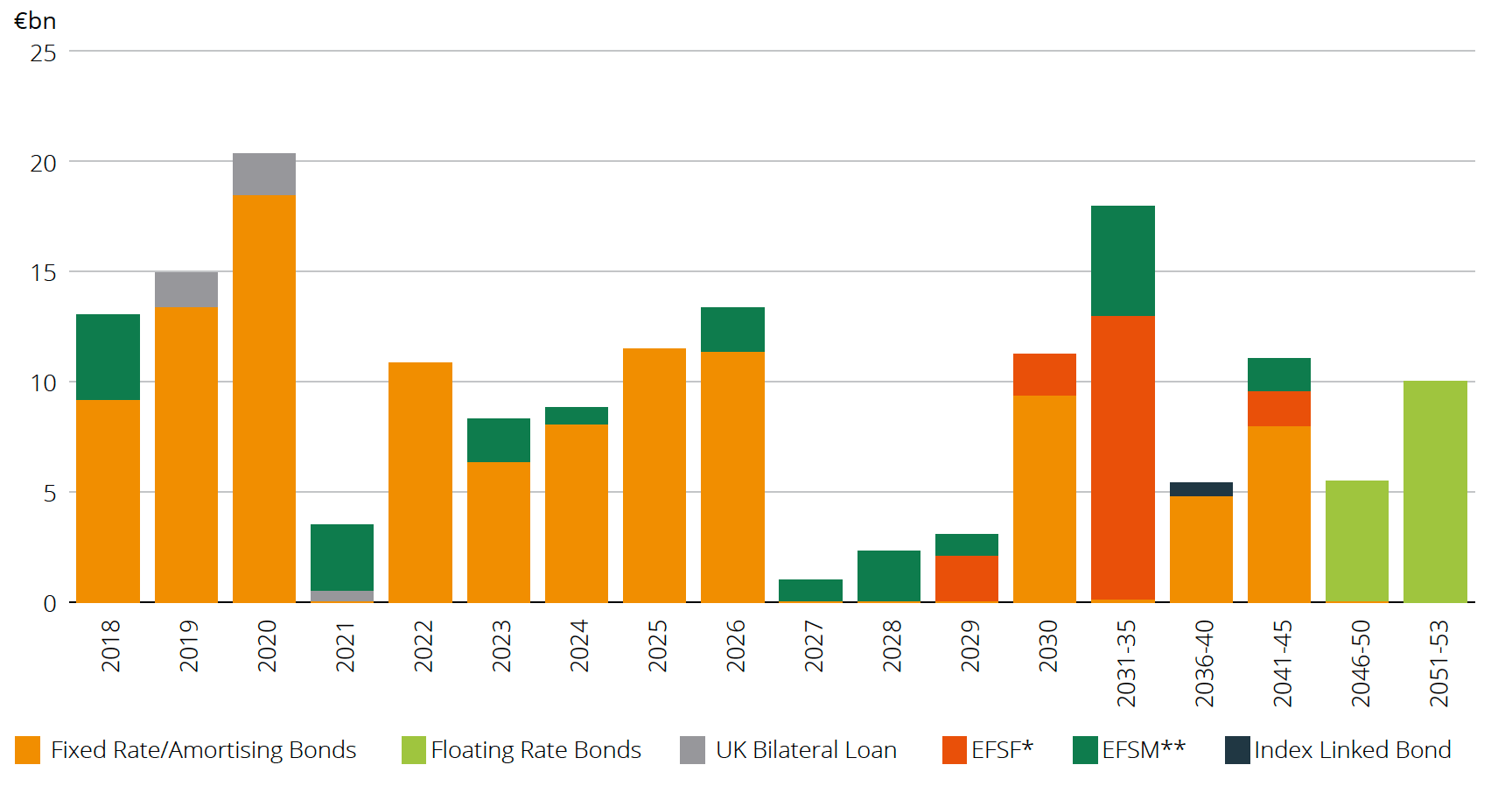

The National Debt maturity profile has improved significantly in recent years. The NTMA has taken steps to reduce the refinancing risk of the large volume of debt maturities arising over the 2018-2020 period. This was achieved through a combination of bond switches, cash pre-funding and the repayment of the IMF and Swedish and Danish bilateral loan facilities. As a result, the refinancing requirement for these years has been almost cut in half. Outstanding maturities have reduced from €60bn to less than €44bn since end-November 2014. When cash balances are taken into account, this is further reduced to close to €30bn.

The weighted average maturity of Ireland’s long-term marketable and official debt is estimated at 11.2 years at end-2017.

Maturity Profile of Ireland’s Long-Term Marketable and Official Debt at End-2017

Notes:

*EFSF loans reflect maturity extensions agreed in June 2013.

**EFSM loans are also subject to maturity extensions agreed in 2013. It is not expected that Ireland will have to refinance any of its EFSM loans before 2027. However, the revised maturity dates of individual EFSM loans will only be determined as they approach their original maturity dates. The chart above reflects both original and revised maturity dates of individual EFSM loans.

DEBT SERVICE COSTS

The NTMA’s primary debt management objectives are to ensure adequate liquidity for the Exchequer and to optimise debt service costs over the medium term.

The cash interest cost of the National Debt in 2017 was €6,092m, 9.6% below the corresponding figure for 2016 and close to 20% below the 2014 peak. The main reason behind the sharp reduction over this period is the early repayment of the IMF loan facility and its replacement with cheaper, long-term, market funding. The 2017 interest bill was 3.2% lower than estimated in Budget 2017 reflecting the favourable interest rate and funding environment evident throughout much of the year.

Interest on the National Debt accounted for 12.0% of Exchequer tax revenue in 2017 compared with 14.1% in 2016 and 15.3% in 2015.

IRISH GOVERNMENT BOND MARKET

At end-2017, Ireland’s benchmark bond curve had a range of maturities, extending to 2045.

Irish Government Fixed Rate Treasury Bonds

| Bond | Maturity Date | Outstanding End-2017 €m* |

|---|---|---|

| 4.5% Treasury Bond 2018 | 18 October 2018 | 8,835 |

| 4.4% Treasury Bond 2019 | 18 June 2019 | 7,235 |

| 5.9% Treasury Bond 2019 | 18 October 2019 | 6,110 |

| 4.5% Treasury Bond 2020 | 18 April 2020 | 10,870 |

| 5.0% Treasury Bond 2020 | 18 October 2020 | 7,573 |

| 0.8% Treasury Bond 2022 | 15 March 2022 | 6,828 |

| 0.0% Treasury Bond 2022 | 18 October 2022 | 4,000 |

| 3.9% Treasury Bond 2023 | 20 March 2023 | 6,308 |

| 3.4% Treasury Bond 2024 | 18 March 2024 | 8,031 |

| 5.4% Treasury Bond 2025 | 13 March 2025 | 11,490 |

| 1.0% Treasury Bond 2026 | 15 May 2026 | 11,319 |

| 2.4% Treasury Bond 2030 | 15 May 2030 | 9,342 |

| 1.7% Treasury Bond 2037 | 15 May 2037 | 4,686 |

| 2.0% Treasury Bond 2045 | 18 February 2045 | 7,904 |

| *excluding repos. | ||

The Irish Government bond market has a strong primary dealer group, mainly international investment banks with a global reach. The 16 primary dealers have exclusive access to the Irish government bond auctions, and are required to quote continuous prices in Irish benchmark bonds.

During 2017, the NTMA reintroduced dual bond auctions, with a choice of two bonds on offer in each auction. There was also increased use of switching and repo (short-term collateralised borrowing) facilities by primary dealers. Amid regulatory and market changes, there is increased pressure on the primary dealer model. The flexibility in the NTMA’s interaction with its primary dealers assists in their ability to make prices and sell Irish Government bonds.

2017 represented another positive year from a credit ratings perspective. Ireland gained rating upgrades from several rating agencies. Moody’s upgraded to A2 (stable) in September, while Fitch upgraded to A+ (stable) in December. Ireland’s long-term rating is now firmly in the A category with all of the major credit rating agencies. All of the agencies noted in their analysis the continuing Irish economic growth, strengthening public finances and improving metrics in the banking sector.

Ireland’s Sovereign Credit Ratings at End-2017

| Rating Agency | Long-term rating |

Short-term rating |

Outlook |

|---|---|---|---|

| Standard & Poor’s | A+ | A-1 | Stable |

| Moody’s | A2 | P-1 | Stable |

| Fitch Ratings | A+ | F1+ | Stable |

The NTMA continued its extensive programme of investor relations during 2017. It held roadshows across Europe, Asia, and the United States. New centres were visited for the first time, including Madrid and Berlin. There were also positive visits to a number of central banks and sovereign wealth funds, which, following Ireland’s sovereign credit rating upgrades, bought Irish bonds after a long absence.

The NTMA’s strategy has been to focus on longer-term holders of Government debt, increasingly in continental Europe. While Germany and the UK remain the two key centres, Switzerland, Austria and the Nordic countries have become an increasing share of the State’s bond issuance.

The Economics Team participated in numerous conferences and events over the course of the year. In addition, it produces and regularly updates the NTMA investor presentation pack. This covers topics from economic data to updates on Government funding and the banking sector.

This investor relations programme is important in developing long-term relationships with investors. It provides transparency to the market about Ireland’s macroeconomic situation and the NTMA’s funding plans and keeps investors informed of Ireland’s credit status.

- 1The SDR is an international reserve asset created by the IMF. The value of the SDR is based on a basket of five major currencies—the US dollar, the euro, the Chinese renminbi (RMB), the Japanese yen, and the British pound sterling.

- 2GNI* for 2017 not available at time of finalisation of Report.